Estate Planning

Why YOU Need Estate Planning

...and what to do about it.

This statistic is frightening.

According to a recent study, only about 40% of adults have an estate plan.

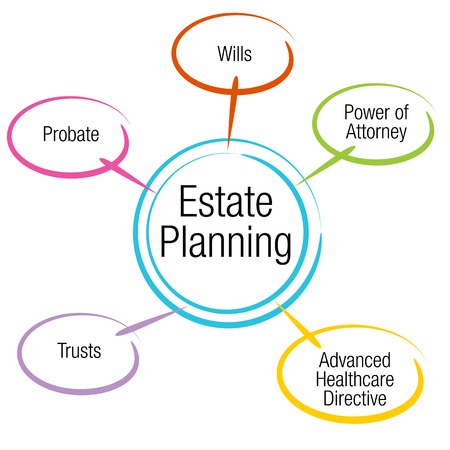

An estate plan is a legal device that communicates the decisions on what happens to a person's wealth and belongings after his or her death. An estate plan can include Wills, Trusts, Powers of Attorney, Living Wills, and a wide spectrum of legal devices to make the estate plan as comprehensive and efficient as possible.

No big deal, you think?

These people may have thought that as well:

- The business owner with a $3 million estate who passed away at age 62 with no will, no spouse, and no kids. Nine siblings left to fight over his assets. Not having an estate plan brought out the worst in all of them. Eighteen months in court with hurt feelings and broken relations.

- The aunt who lived, worked, and died in another state without leaving a will. She intended to leave her assets, including her home, to her life partner, but she never did the paperwork. Her estate was left to nieces and nephews she no longer even spoke with, causing heartbreak for her partner who had to sell their home and move since she could not afford to buy the house from the estate.

- The happily married couple with two young children. Unfortunately, the husband became addicted to gambling and alcohol, they divorced, and he committed suicide. His life insurance named "spouse" as beneficiary, but she was no longer his wife. It ended up going to "next of kin," which was their children, but since they were minors and there was no will that established a trust, the State stepped in to manage the money.

These are all true stories and they happen far more often than you might think.

Are you doing right by your family by investing in your retirement and establishing savings accounts for them?

Sure you are and good for you.

But without a proper estate plan to protect your assets, you're risking their well-being if you're no longer around or able to care for them.

Why Estate Planning?

With a properly devised and implemented estate plan, you establish who manages your assets and how they are distributed after your death, or if you become incapacitated and unable to care for yourself.

It can also direct what happens to your personal health care if you become unable to make those decisions for yourself.

In the unfortunate event that you are unable to manage your finances, an estate plan can designate someone of your choosing, to have access to your assets in order to pay for expenses, such as medical costs and mortgage payments.

More Than Just a Will

An estate plan is wide-ranging protection for you and your family.

Although a will is what most people think of when they think of estate planning, an estate plan can help determine who will take care of your medical care and finances if you ever become unable to do so for yourself. It can also involve funeral decisions, taxes, charitable giving, and business planning as well.

Perhaps even more importantly, an estate plan can help determine who will take care of your minor children in the event both parents were to die. Nominating a guardian for your underage children can allow you to nominate someone who shares your values, while avoiding a "tug-of-war" between well-intentioned family members.

It's a plan that changes with your life events, including, but not limited to changes such as:

- marriage

- divorce

- birth or adoption of a child

- purchasing a home

- significant changes to your health and/or financial situation

- death in the family

Having a trusted estate planning attorney on your side is important to make sure your have someone to discuss your plan and any anticipated changes.

Do I need an estate plan if I'm young and I just started to work?

That's the perfect time to have an estate plan created as you begin to earn and save for your future needs.

If you were to become unable to care for yourself, YOU want to be the one to choose who manages your health care and what happens to your "stuff."

Please know that estate planning is not a "one-size-fits-all" course of action. Your plan when you're just starting out will likely be much different and less complex than when you are married, have a family, and have other assets that you've accumulated.

- ...Or the judge can decide. Without an estate plan, the most important decisions in your life, when you are unable to make them, will most likely be left to a judge to decide who makes them for you. And because so many people don't have an estate plan, there are laws in place to direct the judge's actions. This is called intestate succession. But those laws are not always favorable and it is almost a certainty that the judge's decision won't completely match those that you would have made yourself in creating an estate plan. An estate plan gives you much greater control over what happens to your assets after your death.

What Are My Assets?

Clients sometimes ask what type of items are considered "assets" and they're often surprised to see how long the list is:

- Bank accounts

- Real estate

- Stocks and bonds

- Furniture

- Cars

- Jewelry

- Life insurance proceeds

- Retirement accounts

- Tax refunds due

- Inheritance

- Intellectual Property

- Digital Assets

- Things that may have little to no monetary value but have much sentimental value

- And all the other "stuff" one accumulates during his or her lifetime

How to Provide for Minor Children

Many of my clients ask me for advice on how they should manage their assets to be able to provide for their minor children in the unfortunate event that they become incapacitated or that they predecease their children.

It's important to choose a guardian to care for children until they reach the age of at least 18 years old because in California, a minor child is not legally qualified to care for him or herself and requires an adult to have full legal and physical custody of the child.

Further, a child may need a guardian of her or his estate, if the child inherits money or assets.

However there is more to planning for your child(ren) than simply choosing a guardian, since there are beneficiary designations that can have significant tax consequences.

Powers of Attorney

Another often misunderstood part of estate planning that I discuss thoroughly with my clients are powers of attorney for finances and health care decisions.

A power of attorney is a legal device that gives another person, referred to as an "agent" or "attorney-in-fact," the right and authority to act on your behalf.

Like a will or a trust, the documents should be tailored for your unique situation and wishes. For example, you could elect for the person to be given powers immediately, or to have the powers triggered upon some event which you define, i.e. if you become incapacitated. Further, the powers can be revoked by you at any time thereafter while you still have capacity to do so.

What most don't understand is that the authority granted through a power of attorney ends if you become incapacitated, unless you have a durable power of attorney.

This means that if you were suddenly unable to handle your own affairs, someone you trust, and designated by you, could do so for you.

It's an important distinction to make.

You've Worked Hard for What You've Accomplished

Protect Your Legacy Today!

As you can see - there's a lot for you to protect and preserve for your family, and that's why estate planning is so important for you and for them.

Don't leave your legacy unprotected.

Give me a call at (925) 322-0737 for a free consultation. If you think estate planning makes sense for you, we'll schedule an appointment and talk in person.

If you decide that the timing isn't right at this point, that's okay too. You'll have a better understanding of what an estate plan is and we can talk again in the future when you feel the time is right for you.

Don't wait until it's too late, contact me today!